Insurance enables individuals to protect themselves and their families, in case of any unfortunate happening in the life of the insurer. It will protect your family due to premature death during the tenure.

The importance of an insurance policy is to provide your family with long-term financial security. Insurance policies provide a lump sum of money to financially support.

The importance of insurance grows as you progress through your life stages. Life stages refer to the multiple major stepping stones like marriage, childbirth, retirement, education, etc.

Years of Experience

Customer Served

I am Vineet Suman Saini. We specialize in Wealth Management Services and Insurance Consultancy services for all types of Insurances such as Pension Plans, Health Insurance, Term Plans, Children's education, Marriage, Securing future, Financial Planning, etc.

We offer customized Wealth Solutions that help people to achieve their long-term and medium-term financial goals through effective financial planning. In the last 15 years, we have helped more than 1500 families and individuals in retirement planning, child’s education planning, financial protection against any unforeseen events, etc. We offer a wide range of plans of LIC to suit your diverse needs. Our clients include salaried, businessmen, students, professionals, housewives, government employees, and retired people.

We offer different Insurance Plans such as Pension Plans, Health Insurance, Term Plans, Children's education, Marriage, Securing Future, Financial Planning, etc.

A pension plan or retirement plan is a type of investment plan, which helps you to accumulate a part of your savings over a long-term period so that you can have a secured financial future. A pension Plan helps you to deal with the uncertainties post-retirement and ensures a steady flow of income after retirement. Even if a person has a good amount of savings, a pension plan is nevertheless crucial. A pension plan helps you to create a financial cushion in the long term so that you can ensure a financially sound future after retirement. In a retirement plan, the insured needs to contribute a specific amount regularly until the time of retirement. The accumulated amount is given back to the insured as a pension or annuity at regular intervals of time. The pension plans not only secure the financial future of the individual after retirement but also help an individual deal with the eventualities post-retirement.

Life insurance is the most common form of insurance where you pay the premium for the pre-decided term. If you pass away within the term period, the money you are insured of is given to the family. Unlike term plans, whole life insurance or endowment plans pay upon maturity as well if you outlive the term. One is to pay the premium up to a certain time. The family gets the money upon the untimely death of the insured. Family is what makes a house and they depend on you for everything whether it is money or support, and when you will not there then what will happen to them? The importance of insurance is to provide your family with long-term financial security. Insurance policies provide a lump sum of money to financially support and grow as you progress through your life stages. Life stages refer to the multiple major stepping stones like marriage, childbirth, education, house, world tours, etc.

Health is the greatest blessing for all human beings. Good health is central to human happiness and well-being that contributes significantly to prosperity and wealth. Every aspect of life is dependent on good health. Due to changing, lifestyles health issues have escalated. Every individual is aware that the number of illnesses is increasing day by day and so are the related costs for treatment. A health insurance plan reimburses insured customers for their medical expenses, including treatments, surgeries, hospitalization, and the like which arise from injuries or illnesses, or directly pays out a certain pre-determined sum to the customer. This is an agreement between the insurance company and the customer where the former agrees to guarantee payment or compensation for medical costs if the latter is injured or ill in the future, leading to hospitalization.

The financial advisor is also an educator. Part of the advisor's task is to help you understand what is involved in meeting your future goals. The education process may include detailed help with financial topics. As you advance in your knowledge, the advisor will assist you in understanding complex investments, and insurance. The role involves researching the marketplace and recommending the most appropriate products and services available, ensuring that clients are aware of products that best meet their needs, and then securing a sale. Advisers may specialize in particular products, depending on their clients, such as selling employee pension schemes to companies or offering mortgage, pension, or investment advice to clients. Others are generalists, offering advice to clients in all of these areas, as well as saving plans and insurance.

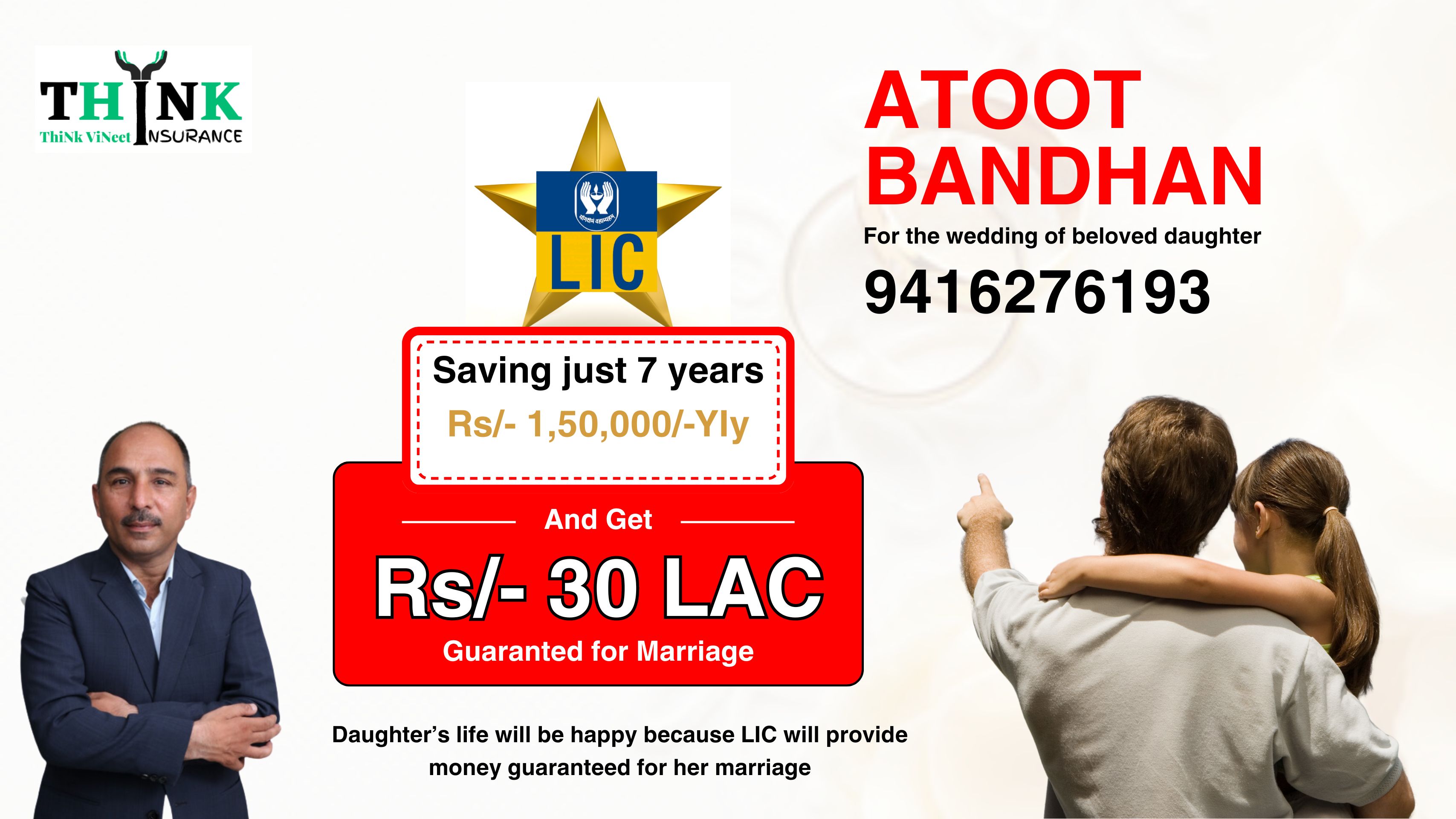

The insurance plan might not seem like a good idea because a child does not have financial value nor are there any liabilities or dependents. Child Education Plans are investment cum insurance policies provided by insurance companies. These are marketed as investments that allow parents to save for their children’s higher education expenses over the policy term while additionally providing financial security to the child in case of the parent’s untimely death. A portion of the premiums paid for the plan is used to provide life cover, while the remainder is invested in Equity or Debt instruments to help save for the higher education requirements of the child. In the case of a Child Education Plan, the life insurance coverage is extended to the parent. These insurance plans mature, and the final payout occurs when the child turns 18.

Life is full of uncertainties. Thus, having a term insurance plan can act as a cushion for a family’s financial security against such uncertainties. However, with an extensive range of term insurance policies available in the market, choosing the right plan can always be a herculean task. To choose the most comprehensive plan there are certain aspects that should be kept in mind. Most insurance seekers often get confused about the policy period, amount of life cover to opt for, what plan to buy, etc. To help our customers make an informed choice, here we have elaborately discussed some tips to choose the best term insurance plan.

.png)

.jpg)

.png)

I am Vineet Suman Saini we specialize in Insurance Consultancy services for all types of Insurance, such as Pension Plans, Health Insurance, Term Loans, Children's Education, Marriage, Securing Future, Financial Planning, etc.

We offer customized Wealth Solutions that help people to achieve their long-term and medium-term financial goals through effective financial planning. In the last 15 years, we have helped more than 1500 families and individuals in retirement planning, child’s education planning, financial protection against any unforeseen events, etc. We offer a wide range of plans of LIC to suit your diverse needs. Our clients include salaried, businessmen, students, professionals, housewives, government employees, and retired people.

Latest News Headlines and Live Updates

.jpg)

The Indian health insurance industry has seen massive transformation in the last few years. Post the COVID-19 crises, policyholders have turned their attention to the importance of having an appropriate health insurance policy. The health insurance market has been growing at a steady pace for the past few years, and it has been the main driver of the non-life insurance industry since March 2020. The retail health insurance market is expected to expand steadily as a result of rising customer awareness, a heightened apprehension of pandemics, and the ongoing introduction of new products by insurers to appeal to a wide variety of customers. However, there are certain coverages in health insurance segments that still confuse policyholders. Take, for example, critical illness coverage. There are several myths in the minds of policyholders about how exactly it is different from health insurance coverage. In this article, we demystify myths and facts about important points for critical illness coverage for policyholders. Myth: Critical illness coverage is not needed for young individuals. Fact: Like health insurance coverage, even critical illness coverage is not related to age, as some serious health ailments might occur even at a younger age. With changes in lifestyles and work cultures coupled with unhealthy eating habits, young individuals are becoming more susceptible to critical illness. So along with comprehensive health insurance coverage, one should have higher coverage even for critical illnesses. Myth: We don’t need critical illness coverage as we have health insurance. Fact: Policyholders should understand that health insurance coverage and critical illness coverage are two different products. A health insurance policy covers hospitalisation expenses when the policyholder falls ill and is admitted to the hospital for more than 24 hours. On the other side, a critical illness insurance policy offers a lump sum pay-out to the policyholder when they are diagnosed with critical ailments like heart attack, cancer, stroke, or paralysis, among others. Myth: All critical illness coverage is covered in my policy. Fact: Like every other insurance policy, policyholders should read the exclusions and inclusions of critical illness coverage before buying them. To give an example, not every form of cancer is covered in every critical illness policy. In some cases, insurers will only pay if the policyholder is diagnosed with stage 2–3 cancer. Partial liver damage may not qualify for insurance either. Myth: All pre-existing illnesses are covered under critical illness coverage. Fact: If the policyholders think that all the pre-existing diseases will be covered in the critical illness coverage, they are thinking wrong. Some life insurance players who provide critical illness riders exclude all pre-existing conditions. However, some players still provide coverage even if the policyholder has a pre-existing medical condition. During the pre-medical testing, if the policyholder is diagnosed with a critical illness, they might have to pay a high premium. Some plans also have a waiting period as well as a surviving period clause in their policy. Therefore, the policyholder should purchase the critical illness plan while they are healthy and then benefit from the lump sum pay-out upon diagnosis. Myth: Critical illness plans are cheaper than health insurance plans. Fact: Someone might assume that critical illness coverage is cheaper, so one should only buy it. Yes, they are sometimes cheaper than health insurance because the risk of a claim being made on the critical illness plan is lower than the risk of a claim on the health insurance plan. It is advisable to spend some time comparing plans and select the one that suits the policyholder in the best possible way. In cases where the policyholder wants a policy that covers the later stages of the illness, they might have to pay higher premiums. If you think that critical illness plans are costly, you can also buy critical illness add-on coverage with your health insurance or life insurance.

.jpg)

How much money is ‘ideal’ for retiring with the same lifestyle? Survey finds Most individuals are cognizant of the need to factor in inflation and rising medical expenses while planning for their life’s new chapter. How much money do you need to retire from work but with the same lifestyle? While there can be no definitive answer to this question as everyone’s lifestyle expenses are different, a survey reveals that many Indians consider Rs 65.4 lakh as an ideal amount for retirement. The survey of over 1100 individuals by ICICI Prudential Life Insurance in association with Quantum Consumer Solutions, reveals that retirement is now being viewed positively as a time full of possibilities. A large number of individuals view retirement as a phase of maintenance, upgradation, and growth. Top concerns and goals The survey reveals some top concerns of working individuals, who are saving/investing for their post-retirement life. • As many as 83% of respondents said continuing with the current lifestyle into their retirement was the topmost priority. • Over three-fifths of the respondents indicated that their retirement goals include enjoying life, staying connected with friends, travelling abroad, feeling financially secure, and having peace of mind in this new chapter of their lives. • Most individuals are cognizant of the need to factor in inflation and rising medical expenses while planning for their life’s new chapter. Inflation, some felt, could impact their standard of living. • Over two-thirds of respondents who participated in the survey said they worry about inflation impacting their retirement savings, and consequently, their lifestyle. • 67% of the respondents highlighted the need to have adequate retirement corpus to take care of medical expenses if stuck with a terminal illness during their retirement. The survey found that currently 11% of the total income of the respondents is channelled towards retirement-specific savings. Most of the respondents consider an average corpus of Rs 65.4 lakh as ideal for retirement. “India’s retirement population is growing rapidly and is projected to show a 41% increase by 2031. Additionally, with increasing life expectancy, a large segment of people will be looking for solutions to plan for a longer retirement,” said Manish Dubey, Chief Marketing Officer, ICICI Prudential Life Insurance.

1.jpg)

Alternatively, the policy should come with a feature like reassure (also called restore or refill), where the sum insured gets replenished an unlimited number of times when it is exhausted," explains Mishra. In the case of cancer, surgery may be followed by chemotherapy or radiotherapy sessions that give rise to small or mid-sized claims repetitively over a considerable period. High sum insured policies or those offering the reassure feature can deal with these costs. In addition, you should have either a fixed-benefit cancer plan or a critical illness plan (which instead of covering a single critical ailment covers up to 45 of them). According to the National Cancer Registry published by the Indian Council of Medical Research, 1.46 million new cancer cases occurred in India in 2022. The incidence of cancer is higher in urban, especially metropolitan, areas due to lifestyle changes, pollution, and so on. With February 4 (observed as World Cancer Day) having just gone by, let us look at how you can insure yourself against this dreaded disease. A high-cost ailment When a person contracts cancer, he or she faces two issues. One, the cost of treating the disease is very high. And two, the ancillary costs that arise also tend to be high. The patient might not be able to do business or may lose his job because of prolonged illness. Those living in smaller towns often have to travel to the metros to get the best treatment. Treatment costs tend to be higher there. An attendant or two has to travel with them. Two covers needed To deal with these problems, a person needs insurance solutions on two fronts. "One, the sum insured on your base indemnity policy (the normal health insurance cover where you are reimbursed for the treatment cost incurred) should be high," says Bhabatosh Mishra, director-underwriting, products and claims, Niva Bupa Health Insurance. Fixed-benefit variant One type of cancer plan is the fixed-benefit plan. A predefined lump sum is paid (irrespective of the expense incurred) as soon as the insured is diagnosed with the disease. "The lump sum amount received from such a plan can be used to meet ancillary costs," says Nayan Goswami, head-sales & service, SANA Insurance Brokers. Siddharth Singhal, business head-health insurance, Policybazaar.com, says that the money received from such a plan can also substitute lost income. Some insurers make staggered pay-outs to mimic regular income flows. At the advanced stage of this disease, many patients go in for palliative care and other alternative treatments. "These lines of treatment are not covered by a regular health insurance plan. Fixed-benefit plans can cover those costs," says Goswami. Indemnity-based plans Indemnity-based cancer plans can help the insured meet the high cost of treatment. People who already have a high cover on their base plans can avoid them. This variant can be useful to those who already have cancer. "A person who has cancer and doesn't have any health insurance will find it difficult to buy a regular hospitalisation cover. An indemnity-based cancer plan may cover them. This way they will at least have coverage for other diseases," says Singhal. Some of these plans may even cover a cancer patient for other variants of cancer (besides the one they already have). Check types of cancer covered These policies have a couple of shortcomings. "The policy document will not say that cancer is covered. It will instead list the types of cancers covered. The longer the list, the better," says Goswami. Types of cancers not mentioned in the list may not be covered. In case of indemnity-based plans, the sum insured provided to people already suffering from cancer may be limited. "It may not exceed Rs 2 lakh-Rs 5 lakh," says Singhal. Managing payouts from two plans -- the base cover and the fixed-benefit cancer plan -- can prove difficult. Money from the latter may only come as reimbursement. Buy early Anyone who can afford to should buy a fixed-benefit plan (or a critical illness plan) to supplement the regular hospitalisation cover. Earlier, there was the notion that this is a geriatric problem, but that is wrong. "The incidence is high both among younger children and the elderly," says Mishra. Buying this cover early is important. "Those who already have pre-cancer lesions or full-blown cancer might find it difficult to get a cover," says Mishra. While a lot of research is happening and new treatments and therapies will become available in the future, they will also be more expensive. "This makes it incumbent on people to have adequate insurance to be able to pay for them," says Mishra. Watch out for survival period clause The survival period clause means the patient must stay alive for a certain period after diagnosis for the pay-out to occur. The survival period may vary from 30 to 90 days. "The lower the survival period, the better," says Goswami. A cancer plan is an add-on cover. It can't be a replacement for a normal health insurance policy. "The regular hospitalisation cover must be purchased first, and then a cancer plan (fixed benefit) should be bought to supplement it," says Goswami. A cancer patient going for an indemnity-based cancer plan should pay heed to a few points. "Try to buy a high sum insured. The waiting period should be minimal and the cashless network should be wide," says Singhal.